38 duration zero coupon bond

What is the duration of a zero coupon bond? - Quora Zero coupon bond can be of any duration , can be from one year to 10 years. It is ordinarily from 3 to 5 years. Zero coupon bonds are issued at a discount with par value paid on redemption, sometimes with a nominal premium. The Macaulay Duration of a Zero-Coupon Bond in Excel Aug 29, 2022 · The Macaulay duration of a zero-coupon bond is equal to the time to maturity of the bond. Simply put, it is a type of fixed-income security that does not pay interest on the principal amount.

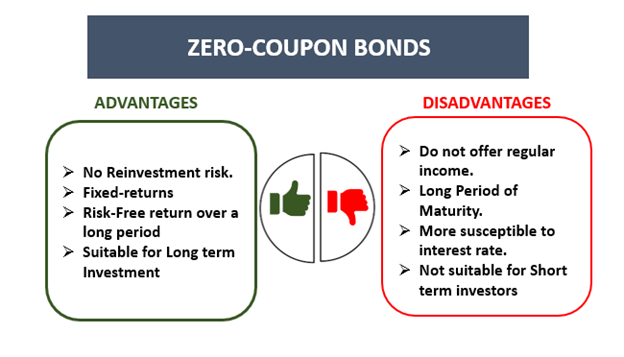

Advantages and Risks of Zero Coupon Treasury Bonds - Investopedia Zero-coupon U.S. Treasury bonds are also known as Treasury zeros, and they often rise dramatically in price when stock prices fall. 1 However, that significant advantage also comes with several unique risks.

Duration zero coupon bond

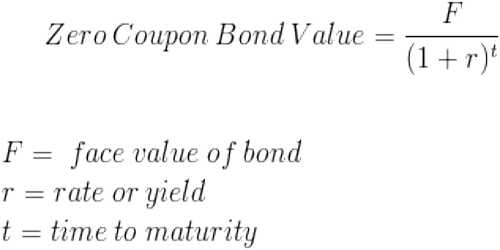

What Is a Zero-Coupon Bond? - Investopedia A zero-coupon bond, also known as an accrual bond, is a debt security that does not pay interest but instead trades at a deep discount, rendering a profit at maturity, when the bond is redeemed for its full face value. Zero-Coupon Bond - Definition, How It Works, Formula Oct 26, 2022 · John is looking to purchase a zero-coupon bond with a face value of $1,000 and 5 years to maturity. The interest rate on the bond is 5% compounded annually. What price will John pay for the bond today? Price of bond = $1,000 / (1+0.05) 5 = $783.53 The price that John will pay for the bond today is $783.53. Example 2: Semi-annual Compounding

Duration zero coupon bond. Zero-Coupon Bond - Definition, How It Works, Formula Oct 26, 2022 · John is looking to purchase a zero-coupon bond with a face value of $1,000 and 5 years to maturity. The interest rate on the bond is 5% compounded annually. What price will John pay for the bond today? Price of bond = $1,000 / (1+0.05) 5 = $783.53 The price that John will pay for the bond today is $783.53. Example 2: Semi-annual Compounding What Is a Zero-Coupon Bond? - Investopedia A zero-coupon bond, also known as an accrual bond, is a debt security that does not pay interest but instead trades at a deep discount, rendering a profit at maturity, when the bond is redeemed for its full face value.

Duration and Zero Coupon Bonds - YouTube

Zero-Coupon Bond Definition & Meaning in Stock Market with ...

Duration model

How to Calculate a Zero Coupon Bond Price | Double Entry ...

Price of a defaultable zero coupon bond price in each time t ...

Bond A is zero-coupon bond paying 100 one year from now. Bond B is a zero-coupon bond paying100 two years from now. Bond C is a 10% coupon bond that pays $10 one year from now and $10 plus the $100 ...

Yields & Prices: Continued - ppt video online download

Aha! Interest rates do matter.

Finding YTM of a Zero Coupon Bond (6.2.1)

Valuing a zero-coupon bond | Mastering Python for Finance ...

A 12.75-year maturity zero-coupon bond selling at a yield to ...

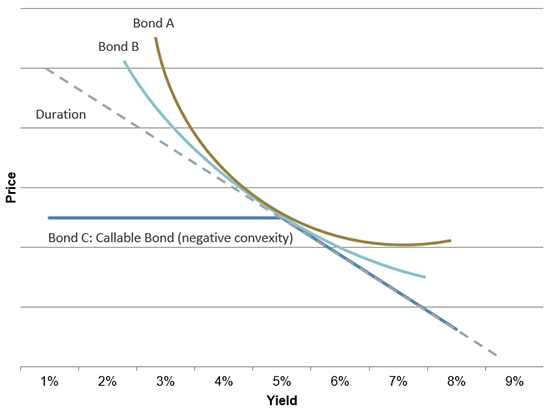

Duration and Convexity in Bond market

Duration & Convexity - Fixed Income Bond Basics | Raymond James

Zero Coupon Bonds Explained (With Examples) - Fervent ...

What Is Duration of a Bond? - TheStreet Definition - TheStreet

Duration | Definition & Examples | InvestingAnswers

WWWFinance - Bond Valuation: Campbell R. Harvey

Zero-Coupon Bond - an overview | ScienceDirect Topics

Are there bonds with zero duration? - Quora

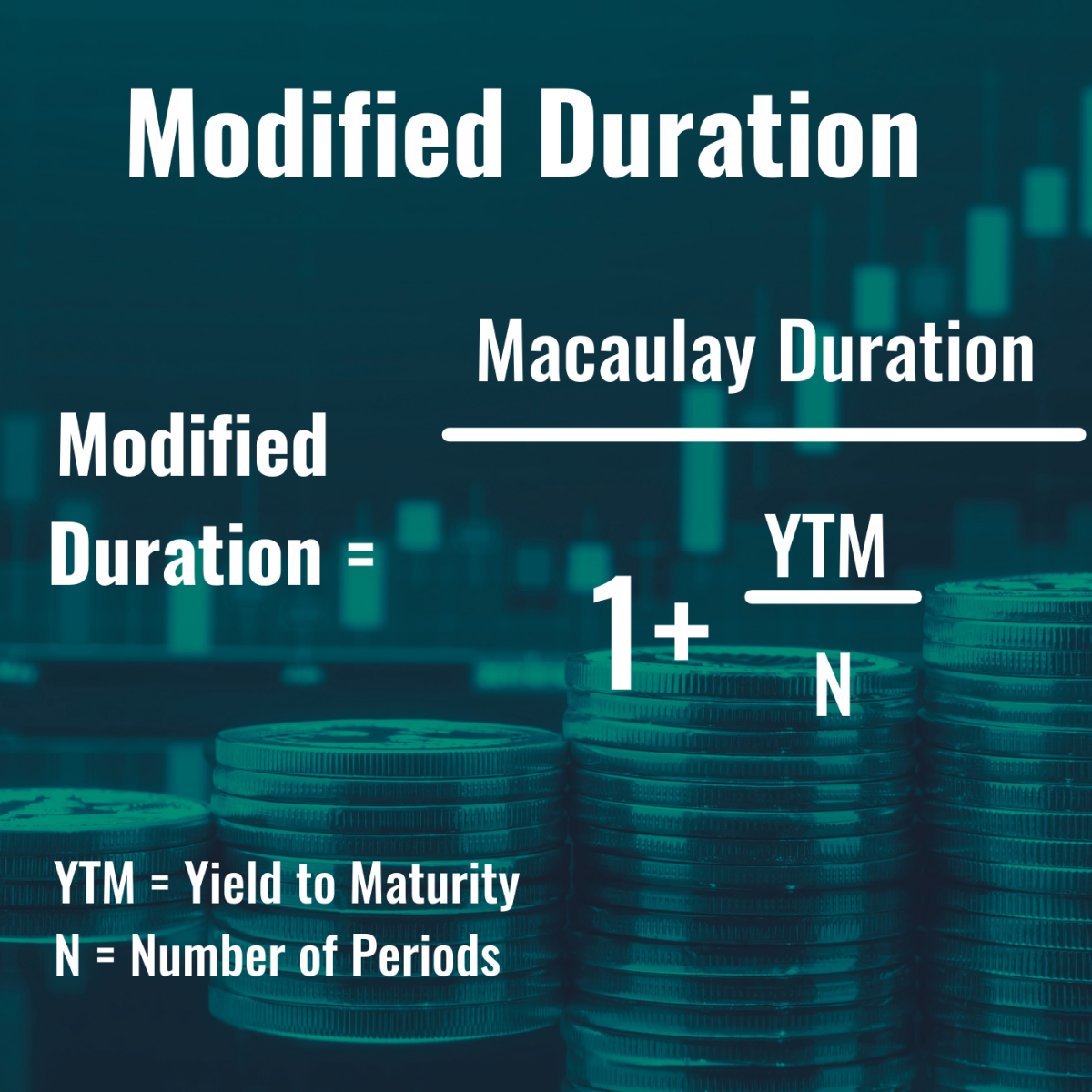

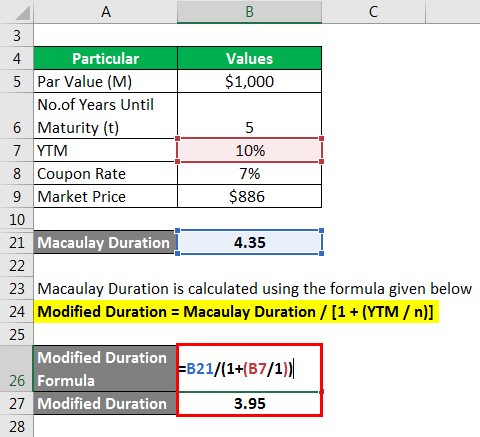

Modified Duration Formula | Calculator (Example with Excel ...

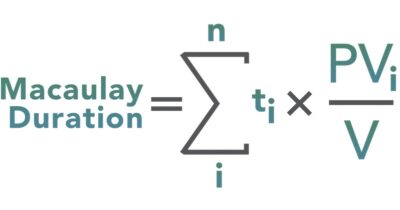

Macaulay Duration

Chapter 4 Bond Price Volatility Chapter Pages 58-85, ppt download

Investment Improvement: Adding Duration to the Toolbox | St ...

Portfolio Duration and its Limitations | CFA Level 1 ...

Impossible Finance — The Perpetual Zero Coupon Bond | by ...

What is the duration of a two-year bond that pays an annual ...

YIELDS TO MATURITY ON ZERO-COUPON RONDS

Duration and Convexity, with Illustrations and Formulas

Duration Analysis

The Key To Duration: Sensitivity To Changing Interest Rates ...

Macaulay's Duration, a Second Look - GlynHolton.com

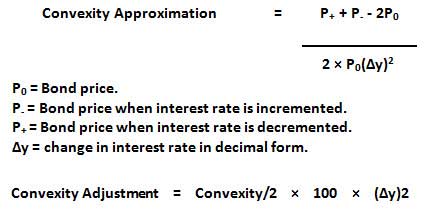

Convexity of a Bond | Formula | Duration | Calculation

Zero Coupon Bond - QS Study

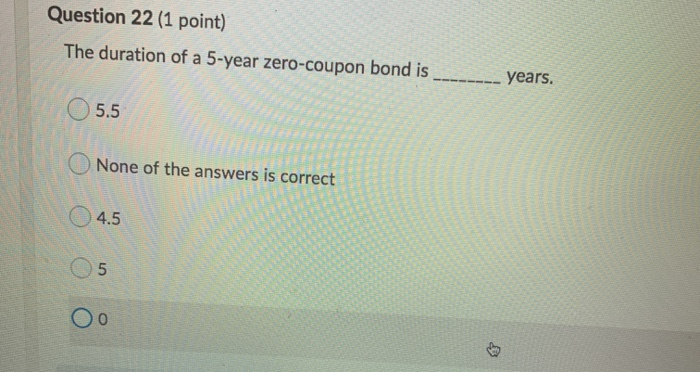

Solved Question 22 (1 point) The duration of a 5-year | Chegg.com

Bond duration - Wikipedia

Duration: Understanding the Relationship Between Bond Prices ...

portfolio management - A question on immunization and ...

Portfolio Duration and its Limitations | CFA Level 1 ...

Post a Comment for "38 duration zero coupon bond"